As EV Giants Push for Greener Batteries, Investors Turn to Next‑Gen Lithium Tech

In the relentless race to secure battery-grade lithium for electric vehicles (EVs), a technological revolution is gaining ground—Direct Lithium Extraction (DLE). A new report by Benchmark Mineral Intelligence projects that the global DLE market will expand at a compound annual growth rate (CAGR) of 19.6% between 2026 and 2036, nearly doubling the pace of overall lithium production growth.

That’s not just a marginal evolution in mining—it’s a fundamental transformation of how one of the world’s most in-demand resources is extracted, refined, and brought to market. For investors looking to get ahead of the next big wave in green tech, DLE is no longer speculative—it’s strategic.

Why This Matters for Investors

The urgency is clear: EV adoption is accelerating globally, with BloombergNEF forecasting that 56% of all passenger vehicles sold by 2040 will be electric. At the same time, traditional lithium extraction—primarily hard-rock mining and brine evaporation—faces growing scrutiny due to its slow processing times, high water use, and large carbon footprint.

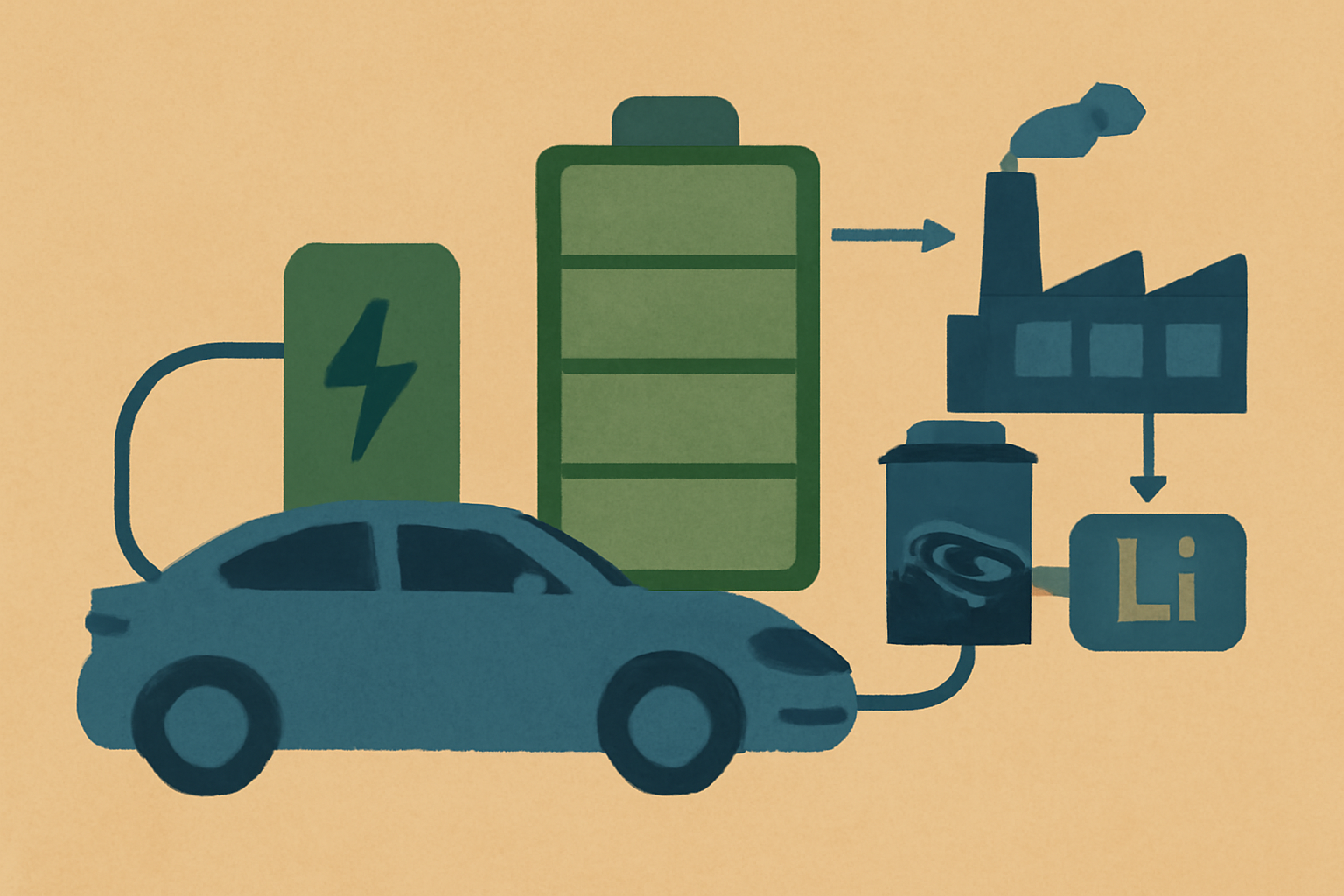

Enter Direct Lithium Extraction, a process that chemically separates lithium from brine using filters, membranes, or solvents—dramatically shortening production time from months to hours, and offering significantly lower environmental impact. Goldman Sachs has described DLE as potentially “transformational for lithium supply chains” in a research note earlier this year.

DLE’s promise is already attracting capital. Companies like Lilac Solutions, backed by Breakthrough Energy Ventures (founded by Bill Gates), and EnergyX, which just closed a $50 million Series B, are positioning themselves as leaders in the space. Public companies such as Standard Lithium (TSXV: SLI) and E3 Lithium (TSXV: ETL) are also deploying DLE technologies in pilot and pre-commercial phases.

Core Analysis: Growth Signals and Strategic Drivers

The growth trajectory for DLE isn’t just theoretical. According to McKinsey & Company, lithium demand is expected to quadruple by 2030, while current extraction methods struggle to keep pace with volume, speed, and ESG expectations. McKinsey’s latest clean tech report highlights DLE as a “priority investment area” for green transition portfolios.

Several key drivers are accelerating DLE’s commercial viability:

- Environmental Regulation Pressure: Governments in Chile, Argentina, and the U.S. are tightening water-use and emissions rules on traditional lithium operations, creating a regulatory tailwind for DLE.

- Onshoring Critical Minerals: The U.S. Inflation Reduction Act and Canada’s Critical Minerals Strategy both promote domestic lithium sourcing, with incentives for clean-tech extraction methods. DLE offers a viable path to North American lithium independence.

- OEM Partnerships: Automakers are moving upstream. General Motors, Ford, and Stellantis have all struck lithium supply deals with DLE firms in the past 12 months. These relationships reduce offtake risk for early-stage producers and signal confidence in the tech.

Future Trends to Watch

- Commercialization Milestones (2026–2028): While pilot plants are proving successful, large-scale commercialization will be the next validation test. Watch for key production announcements from companies like Standard Lithium and Summit Nanotech.

- Strategic M&A Activity: As legacy miners look to integrate DLE into their operations, expect acquisition or joint venture deals targeting tech firms with proven IP and early output capacity.

- Tech Differentiation: Not all DLE methods are equal. Investors should track which technologies (adsorption, solvent extraction, ion exchange) achieve the best lithium recovery rates, cost metrics, and ESG scores.

- Government Funding & Permitting Fast Lanes: Jurisdictions offering expedited permitting for DLE operations—particularly in Canada and the southwestern U.S.—may emerge as hubs for new lithium supply.

Key Investment Insight

Investors looking to ride the DLE wave should consider a diversified approach:

- Early-stage DLE developers with proven pilot results (e.g., Standard Lithium, E3 Lithium) offer high-risk/high-reward upside.

- Chemical tech firms licensing membrane or solvent systems to DLE operations could be hidden winners.

- ETF exposure through clean tech and critical mineral ETFs (e.g., LIT, BATT) provides broader access with lower volatility.

Given the convergence of policy support, environmental necessity, and capital inflows, DLE is well on its way to becoming a foundational component of the EV supply chain. For investors with vision—and patience—the next decade could be transformative.

Stay informed with MoneyNews.Today—your daily edge on the fastest-moving sectors shaping tomorrow’s investment landscape.