The global markets kicked off the week on a high note, with Wall Street hitting fresh record levels as optimism builds around a potential trade breakthrough between the United States and China. Investor sentiment was further buoyed by the anticipation of a critical week for technology earnings — one that could define market direction into year-end.

Semiconductors and AI-hardware giants led the rally, reflecting growing investor conviction in the resilience of the technology sector despite lingering macroeconomic and policy risks.

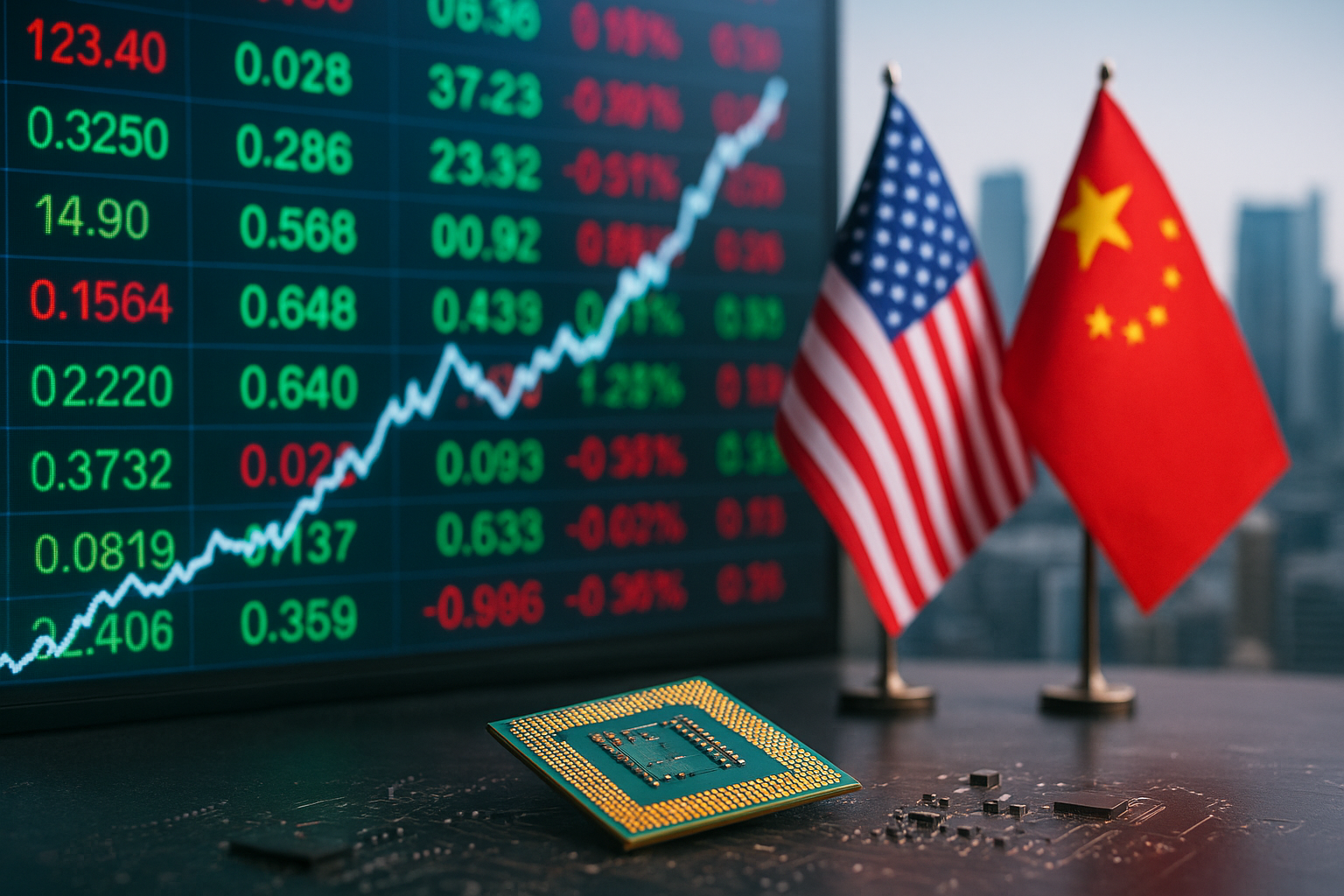

Market Rally Fueled by Renewed U.S.–China Trade Optimism

According to Reuters (Oct 27, 2025), the S&P 500 and Nasdaq Composite both reached new highs as officials from Washington and Beijing signaled progress toward a “limited trade framework” that could ease restrictions on advanced semiconductor exports and AI components. The talks — seen as the first constructive engagement between the two nations in months — have reignited confidence in the global tech supply chain.

Shares of chipmakers like Nvidia ($NVDA), Advanced Micro Devices ($AMD), and Taiwan Semiconductor Manufacturing Co. ($TSM) surged between 2% and 5% on Monday, while AI infrastructure players such as Broadcom ($AVGO) and Marvell Technology ($MRVL) also climbed amid expectations of stronger demand forecasts.

“The market is rewarding any sign of de-escalation in trade tensions because so much of the semiconductor story depends on open global supply chains,” said Daniel Morris, Chief Market Strategist at BNP Paribas. “If these talks hold, the AI hardware cycle could extend well into 2026.”

Why This Matters for Investors

The rally highlights a significant shift in investor psychology — from caution over elevated valuations to optimism fueled by geopolitical and earnings catalysts.

Tech stocks have been the backbone of the 2025 equity market rebound, contributing more than 60% of the S&P 500’s total gains this year, according to data from Bloomberg. The “Magnificent Seven” — Apple ($AAPL), Microsoft ($MSFT), Nvidia ($NVDA), Amazon ($AMZN), Meta ($META), Alphabet ($GOOGL), and Tesla ($TSLA) — now collectively account for over 30% of the index’s market cap.

With five of these giants set to report earnings this week, analysts are watching closely for guidance on cloud spending, AI infrastructure expansion, and capital expenditure trends.

“The upcoming earnings will be a real test for the sustainability of this rally,” noted Liz Ann Sonders, Chief Investment Strategist at Charles Schwab. “Investors need to look beyond the headline beats — margins, AI adoption rates, and data-center utilization will tell the true story.”

The AI and Semiconductor Nexus

AI continues to drive the narrative for the technology sector. Capital expenditure in AI data centers is expected to top $3 trillion globally by 2030, according to McKinsey & Co., with U.S. firms commanding nearly half of that total.

The current rally has been particularly strong in semiconductor infrastructure, as firms race to meet demand for advanced AI chips and compute power. Companies like Nvidia and Broadcom remain key beneficiaries, but second-tier chip design and manufacturing firms are also seeing renewed investor interest as the “AI ecosystem” broadens.

However, not all signals are green. Policy risk remains a wildcard — particularly if U.S. export controls tighten again or if Chinese retaliation affects supply chains. For investors, the short-term exuberance may mask underlying volatility tied to policy outcomes.

Future Trends to Watch

- Earnings Season Volatility: Expect sharp movements as major tech firms release Q3 results. Investors should monitor not just revenue growth but forward guidance, particularly around AI infrastructure and global demand.

- AI Capex Expansion: Tech giants are expected to maintain record levels of capital spending into 2026. Companies enabling data-center buildouts — from chipmakers to power infrastructure — are positioned for strong tailwinds.

- Trade Policy Clarity: Any formal agreement between the U.S. and China could reprice semiconductor valuations higher, while renewed restrictions would likely trigger sector-wide corrections.

- Shift Toward Efficiency: With rates expected to stay elevated, analysts anticipate a market rotation toward companies showing durable earnings growth and operational efficiency rather than speculative AI narratives.

Key Investment Insight

The market’s response underscores that momentum in technology remains real and broad-based, but it’s also becoming increasingly selective. Investors seeking exposure should focus on high-quality firms with diversified AI infrastructure exposure and solid balance sheets.

Portfolio diversification — through both AI hardware leaders and supporting industries such as cloud infrastructure and energy-efficient chip manufacturing — remains the best hedge against policy and earnings volatility.

As global trade dialogue and corporate earnings converge this week, investors will gain crucial insight into whether the 2025 tech rally has further room to run — or if profit-taking and policy shocks could bring volatility back to the forefront.

Stay updated with MoneyNews.Today for daily coverage of market-moving trends shaping the future of investing.