The global artificial intelligence race just entered a new phase—and investors around the world are paying close attention.

China is reportedly preparing a massive 2 trillion yuan ($295 billion) national investment initiative aimed at accelerating the country’s artificial intelligence capabilities. According to reports from Bloomberg, cited by Reuters, the plan would direct funding toward AI data centers, advanced computing infrastructure, quantum technologies, and humanoid robotics, while prioritizing domestic technology champions.

The announcement arrives at a pivotal moment for global markets. AI-related stocks have driven much of the equity market’s gains over the past two years, with investors pouring capital into semiconductor manufacturers, cloud computing providers, data-center operators, and energy infrastructure companies. China’s latest move signals that the competition for AI leadership is no longer centered solely in Silicon Valley—it is becoming a strategic contest between the world’s two largest economies.

For investors, the implications extend far beyond technology stocks.

A New Chapter in the Global AI Race

Artificial intelligence has evolved from a technology trend into a national economic and security priority.

The United States has led much of the recent AI boom through companies such as Nvidia, Microsoft, OpenAI, Alphabet, and Amazon. Massive investments in AI chips, cloud computing, and large language models have created trillions of dollars in market value and transformed investor expectations regarding future economic growth.

China’s proposed AI infrastructure initiative appears designed to narrow that gap.

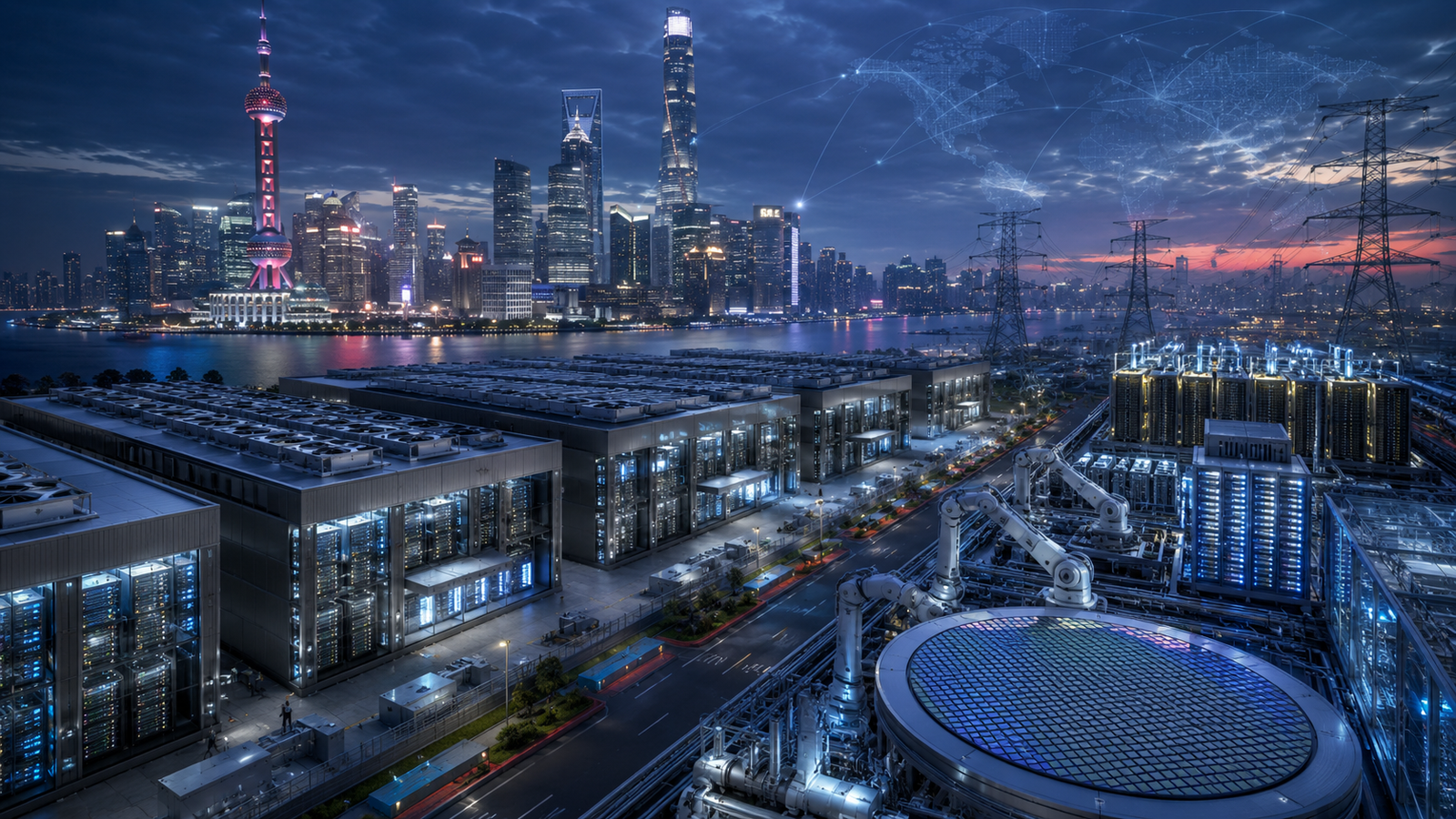

Reports indicate that the investment package would support the development of domestic AI ecosystems, including advanced data centers, high-performance computing networks, semiconductor technologies, quantum computing research, and next-generation robotics. Chinese technology companies, including Huawei and other domestic hardware providers, are expected to play significant roles in the initiative.

The scale of the proposal is particularly noteworthy. At approximately $295 billion, the planned investment would rank among the largest technology-focused government initiatives in modern history.

For investors, the message is clear: AI spending is accelerating globally rather than slowing down.

Why Infrastructure Is Becoming the Next AI Battleground

Much of the public attention surrounding AI has focused on software applications such as ChatGPT, AI assistants, and generative content tools.

However, industry experts increasingly emphasize that the true AI opportunity may lie in the infrastructure powering these applications.

Training and deploying advanced AI systems require enormous amounts of computing power, specialized semiconductors, data-center capacity, and electricity. As AI adoption expands across industries, demand for these foundational assets continues to rise.

According to industry estimates from organizations including McKinsey and the International Energy Agency, AI-driven computing demand could significantly increase global electricity consumption over the coming decade. Data centers are already emerging as one of the fastest-growing sources of power demand in developed markets.

China’s proposed initiative reinforces this trend by focusing heavily on infrastructure rather than consumer-facing applications alone.

Investors should view the announcement as another signal that the AI investment cycle remains in its early stages.

Semiconductor Demand Could Receive Another Boost

The semiconductor industry remains at the center of the global AI economy.

Over the past two years, companies producing advanced graphics processing units (GPUs), memory chips, networking equipment, and AI accelerators have experienced unprecedented demand.

China’s investment plans could create additional demand for domestic chipmakers while also increasing global competition across the semiconductor supply chain.

Although U.S. export restrictions continue to limit China’s access to some advanced AI chips, Beijing has increasingly prioritized self-sufficiency in critical technologies. This has created opportunities for Chinese firms to develop alternatives while encouraging greater investment throughout the semiconductor ecosystem.

For investors, the broader takeaway is that global AI spending remains robust regardless of geopolitical tensions.

Companies involved in chip manufacturing equipment, advanced packaging, memory technologies, networking infrastructure, and AI hardware may continue benefiting from long-term demand growth.

Quantum Computing and Robotics Move Into Focus

While much of the market remains focused on AI software, China’s initiative also highlights two sectors that could become major investment themes over the next decade: quantum computing and humanoid robotics.

Quantum computing has the potential to revolutionize industries ranging from cybersecurity and pharmaceuticals to materials science and financial modeling. Governments and corporations worldwide are increasing investments in the field as they seek technological advantages.

Meanwhile, humanoid robotics is attracting growing interest from technology companies seeking to automate manufacturing, logistics, healthcare, and service industries.

Analysts increasingly view robotics as a natural extension of the AI revolution. As machine learning capabilities improve, robots become more capable of performing complex physical tasks traditionally reserved for human workers.

Investors searching for the next phase of AI-related growth may find opportunities in companies operating within these emerging sectors.

Geopolitical Competition Is Becoming an Investment Theme

China’s AI infrastructure initiative also underscores a broader geopolitical reality.

Technology leadership is increasingly being treated as a strategic national objective rather than simply a commercial opportunity.

The United States has introduced export controls, domestic semiconductor incentives, and industrial policies designed to strengthen its technological position. China’s latest investment proposal appears to be part of a broader effort to achieve greater technological independence while reducing reliance on foreign suppliers.

As a result, investors are increasingly evaluating companies through the lens of geopolitical competition.

Firms that provide critical AI infrastructure, domestic manufacturing capabilities, cybersecurity solutions, and advanced semiconductor technologies could benefit from continued government support and strategic investment.

At the same time, increased competition may create volatility across global technology markets as policymakers implement new regulations, subsidies, and trade restrictions.

What Investors Should Watch Next

Several key developments could determine how markets respond to China’s AI initiative in the months ahead.

First, investors should monitor implementation details and funding mechanisms associated with the reported investment plan. Large government initiatives often evolve over time, and specific allocations may reveal which sectors stand to benefit most.

Second, developments in semiconductor policy remain critical. Any changes to export controls, technology partnerships, or domestic manufacturing incentives could have significant implications for global AI supply chains.

Third, investors should watch data-center construction activity and power infrastructure investment trends. The AI revolution increasingly depends on electricity availability, creating opportunities beyond traditional technology sectors.

Finally, the competitive response from U.S. companies and policymakers may become a major market catalyst. Additional incentives, infrastructure programs, or AI-related investments could further accelerate global spending.

Key Investment Insight

China’s reported $295 billion AI infrastructure initiative reinforces a growing reality: the AI investment cycle is expanding rather than slowing. While software applications capture headlines, the biggest long-term opportunities may lie in the infrastructure supporting artificial intelligence—including semiconductors, data centers, networking equipment, power generation, grid modernization, quantum computing, and robotics.

Investors should focus on companies positioned to benefit from rising global AI spending rather than viewing the opportunity through a single-country lens. As competition between the United States and China intensifies, the winners may include infrastructure providers, equipment manufacturers, and technology suppliers serving both ecosystems.

The AI race is no longer just a technology story—it is becoming one of the defining economic and investment themes of the decade.

Stay informed with MoneyNews.Today for daily investor insights, market-moving developments, and in-depth analysis of the trends shaping the future of global investing.