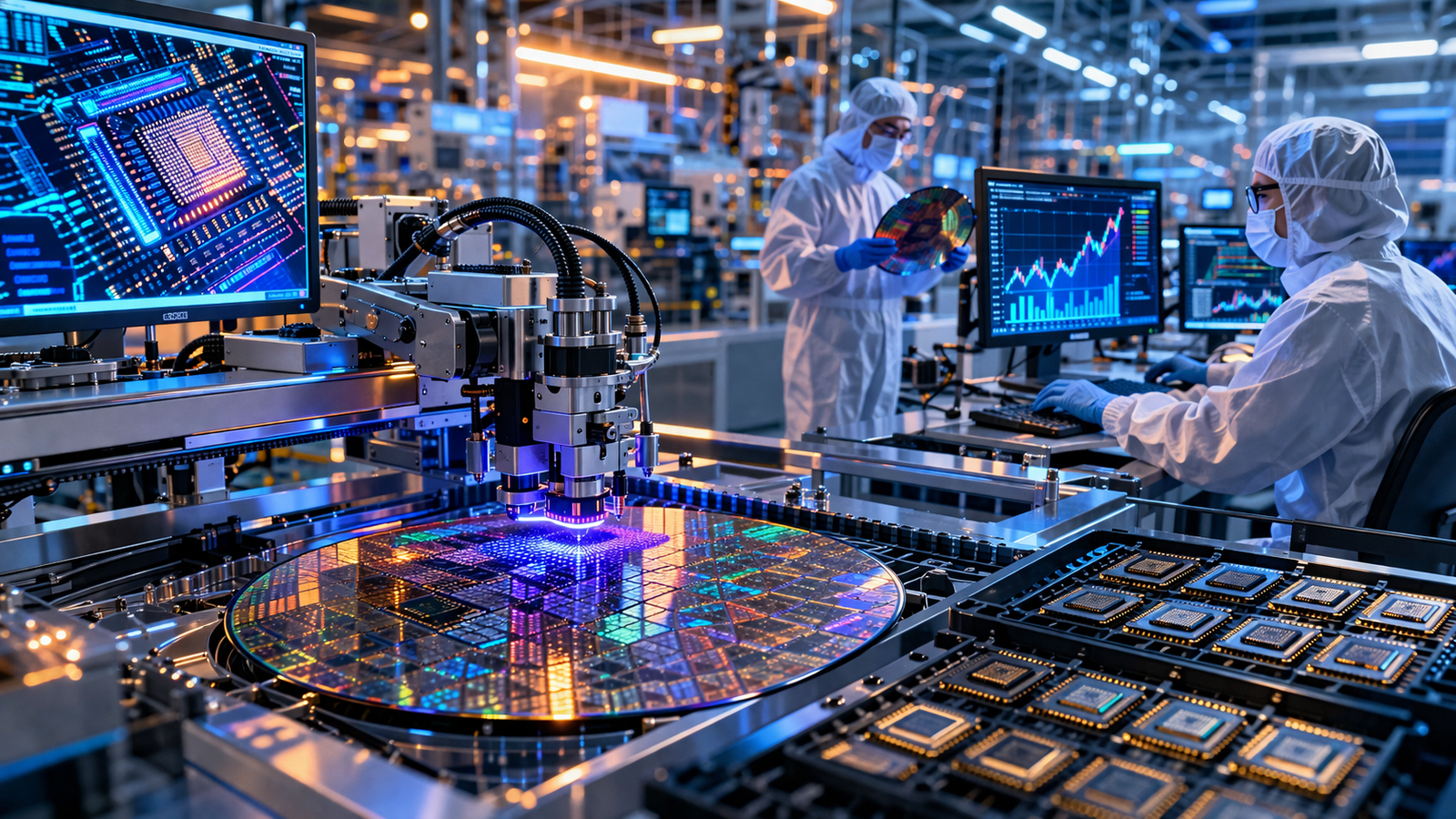

The AI boom is no longer just lifting software companies—it’s igniting a powerful rally at the very foundation of the digital economy: semiconductors.

As artificial intelligence adoption accelerates across industries, demand for high-performance chips has surged to unprecedented levels. From hyperscale data centers to enterprise AI deployments, the need for advanced processors is overwhelming supply chains that are still catching up from years of underinvestment and complexity.

The result is a clear market signal: semiconductor stocks are extending gains, driven by persistent demand, constrained supply, and record order backlogs. According to recent reporting from Bloomberg and The Information (April 15, 2026), foundries and advanced packaging providers are operating at capacity, with demand showing little sign of slowing.

For investors, this is more than a cyclical upswing—it is a structural shift that is redefining the semiconductor industry as the central pillar of the AI economy.

The AI Boom Is Driving a New Chip Supercycle

The semiconductor industry has always been cyclical, tied to consumer electronics, enterprise spending, and macroeconomic trends. But AI is introducing a new dynamic—one that is less cyclical and more structural.

AI workloads require:

- High-performance GPUs and accelerators

- Advanced memory solutions

- Cutting-edge manufacturing processes

Unlike traditional computing demand, AI infrastructure buildouts are:

- Capital-intensive

- Long-term in nature

- Mission-critical for competitive positioning

This creates sustained demand that extends beyond typical upgrade cycles.

In effect, the industry is entering what many analysts are calling a “chip supercycle”, driven by AI rather than consumer demand.

Supply Constraints Are the Defining Factor

While demand is surging, supply remains the limiting factor—and that is where the investment opportunity becomes most compelling.

Several bottlenecks are constraining semiconductor production:

Advanced Node Manufacturing Limits

Producing AI chips requires leading-edge fabrication technologies, often at 5nm and below. Only a handful of foundries globally have the capability to operate at this level, creating a highly concentrated supply base.

Advanced Packaging Bottlenecks

AI chips increasingly rely on sophisticated packaging techniques, such as chiplets and 3D stacking. Capacity in this segment is limited, leading to extended lead times and order backlogs.

Equipment and Materials Constraints

Semiconductor manufacturing depends on highly specialized equipment and materials, many of which have long production cycles and limited suppliers.

These constraints are not easily resolved. Building new fabrication plants and expanding capacity can take years and require billions of dollars in investment.

As a result, the imbalance between supply and demand is likely to persist—supporting pricing power across the industry.

Why This Matters for Investors

The current environment is reshaping how investors should approach semiconductor exposure.

1. The Value Chain Is Expanding

The AI semiconductor ecosystem extends far beyond chip designers. It includes:

- Foundries

- Equipment manufacturers

- Materials suppliers

- Packaging and testing firms

While headline names often capture attention, second-tier players within this ecosystem are increasingly benefiting from capacity constraints.

For example:

- Equipment makers supplying lithography and fabrication tools

- Companies specializing in advanced packaging technologies

- Suppliers of critical materials like wafers and chemicals

These segments are seeing strong demand, often with less valuation premium compared to leading chip designers.

2. Pricing Power Is Strengthening

In an environment where demand exceeds supply, pricing power shifts to producers.

This is already evident in:

- Premium pricing for AI GPUs and accelerators

- Long-term supply agreements locking in favorable terms

- Increased margins for foundries and suppliers

For investors, this dynamic supports earnings growth and justifies elevated valuations—at least in the near to medium term.

3. Capital Expenditure Cycles Are Accelerating

Semiconductor companies are responding to demand by ramping up capital expenditures.

New fabrication plants, expansion of existing facilities, and investments in advanced technologies are all underway. Governments in the U.S. and allied countries are also supporting domestic chip production through subsidies and incentives.

This creates a ripple effect across industries, benefiting:

- Construction and engineering firms

- Industrial equipment manufacturers

- Energy providers supporting high-power fabs

The semiconductor boom is, therefore, not isolated—it is driving a broader industrial investment cycle.

The Strategic Importance of Semiconductor Supply Chains

Beyond financial performance, semiconductors are becoming a strategic asset.

Governments are increasingly focused on:

- Reducing reliance on foreign supply chains

- Securing access to critical technologies

- Building domestic manufacturing capabilities

This geopolitical dimension adds another layer to the investment thesis.

Policy support, including funding and incentives, is likely to continue—providing a tailwind for companies involved in semiconductor manufacturing and infrastructure.

Future Trends to Watch

As the AI-driven semiconductor boom evolves, several key trends will shape the market:

Expansion of Advanced Packaging Capacity

Given current bottlenecks, significant investment is expected in packaging technologies, which could unlock additional performance gains and alleviate supply constraints.

Rise of Alternative Chip Architectures

To optimize AI workloads, companies are developing specialized chips and architectures, potentially reshaping competitive dynamics within the industry.

Increased Vertical Integration

Tech giants may seek greater control over chip supply by investing directly in design, manufacturing partnerships, or even in-house production capabilities.

Continued Government Intervention

National security and economic competitiveness will keep semiconductors at the center of policy discussions, influencing funding and regulatory frameworks.

Why This Is More Than Just a Rally

While semiconductor stocks are currently benefiting from strong momentum, the underlying drivers suggest this is not a short-lived trend.

The convergence of:

- AI adoption

- Supply constraints

- Strategic importance

is creating a unique environment where semiconductors are not just cyclical assets, but foundational infrastructure for the digital economy.

This distinction is critical for investors. It shifts the narrative from short-term trading opportunities to long-term structural positioning.

Key Investment Insight

The AI trade is increasingly becoming a semiconductor capacity story.

For investors, this means looking beyond the obvious winners and identifying opportunities across the broader ecosystem:

- Foundries with limited but critical capacity

- Equipment manufacturers enabling production expansion

- Packaging and materials companies addressing key bottlenecks

These segments may offer compelling upside as the industry works to close the gap between supply and demand.

At the same time, investors should remain mindful of risks, including:

- Overcapacity in the long term

- Geopolitical tensions

- Execution challenges in large-scale projects

Balancing these factors will be key to navigating the semiconductor landscape.

The rally in semiconductor stocks is a reflection of a deeper transformation underway in the global economy. As AI continues to scale, the demand for chips will remain a defining force—reshaping industries, supply chains, and investment strategies.

For those paying attention, this is not just a trend—it is a structural shift with far-reaching implications.

Stay with MoneyNews.Today for daily, in-depth analysis that helps you uncover emerging opportunities, understand market dynamics, and stay ahead in a rapidly evolving investment landscape.