Global markets are entering another period where geopolitics may matter just as much as earnings reports and economic data. Investors across Wall Street are closely monitoring two major international developments that could significantly shape financial markets in the months ahead: a highly anticipated meeting between Donald Trump and Chinese President Xi Jinping, and increasingly fragile U.S.-Iran negotiations that are fueling volatility in energy markets.

At a time when artificial intelligence, semiconductors, critical minerals, and global supply chains are already reshaping investment strategies, geopolitical tensions are adding another layer of complexity to the market outlook. Traders, hedge funds, and institutional investors are now weighing how trade policy, AI export restrictions, Taiwan tensions, and energy security could impact inflation, commodity prices, and corporate profitability throughout 2026.

The growing importance of geopolitics reflects a broader transformation in global investing. Political negotiations are no longer isolated diplomatic events — they are increasingly direct market catalysts capable of moving equities, oil prices, semiconductor stocks, and currency markets within hours.

For investors, understanding the intersection between politics, technology, and global trade is becoming essential.

Markets Focus on Trump-Xi Meeting

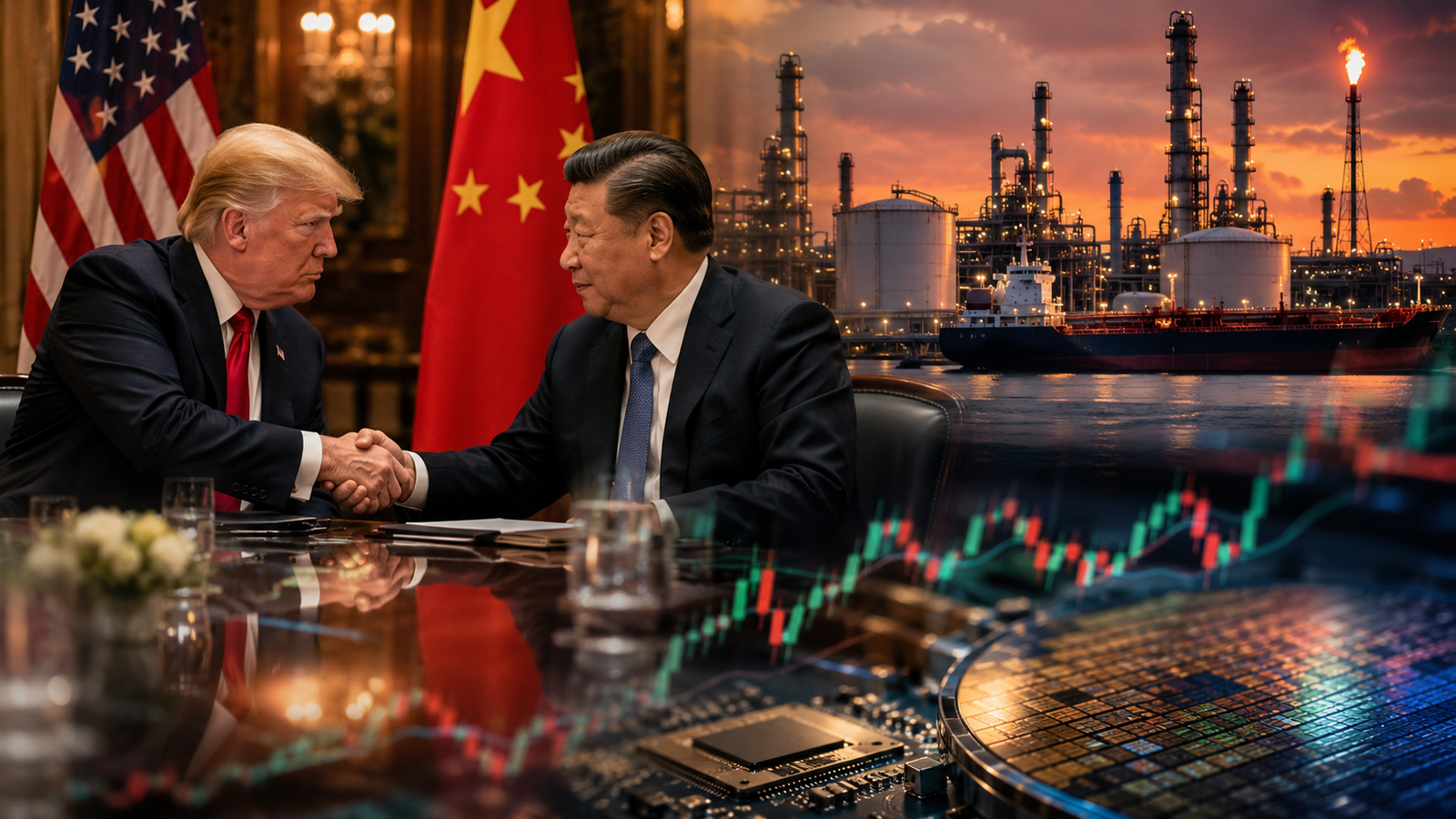

One of the biggest geopolitical events capturing investor attention is the expected meeting between Donald Trump and Xi Jinping.

According to Reuters and several financial media reports, markets are closely watching whether discussions between the United States and China can ease growing tensions surrounding trade restrictions, artificial intelligence development, semiconductor exports, and strategic mineral supply chains.

The U.S.-China relationship remains one of the most important drivers of global economic sentiment because the two countries are deeply interconnected across manufacturing, technology, energy, and financial markets.

Recent years have seen growing friction over several critical issues:

- Semiconductor export controls

- AI technology restrictions

- Taiwan-related military tensions

- Supply-chain security

- Tariffs and trade imbalances

- Strategic mineral access

For investors, the upcoming discussions could influence multiple sectors simultaneously.

Semiconductor companies, AI infrastructure firms, industrial manufacturers, and multinational technology corporations are particularly sensitive to changes in U.S.-China policy. Even small shifts in export rules or trade agreements can significantly impact earnings expectations and supply-chain costs.

Markets are especially focused on whether the talks produce any progress regarding AI chip restrictions and advanced semiconductor exports.

The Biden-era restrictions on high-performance AI chips and semiconductor manufacturing equipment created major disruptions for global technology firms. Investors are now debating whether Trump’s administration could maintain, expand, or modify those policies moving forward.

That uncertainty is contributing to heightened volatility across the semiconductor sector.

AI and Semiconductors Are at the Center of the Conflict

Artificial intelligence has transformed from a technology trend into a geopolitical battleground.

Governments increasingly view AI leadership as a matter of national security and economic dominance. The race to control advanced AI infrastructure, semiconductor manufacturing, and computing power is reshaping trade policy across the globe.

Nvidia, AMD, Intel, Taiwan Semiconductor Manufacturing Company, and other semiconductor leaders are now operating at the center of both technological innovation and geopolitical strategy.

According to Bloomberg and Reuters, investors are particularly concerned about how future AI export controls could affect semiconductor revenues, cloud infrastructure expansion, and global technology supply chains.

China remains one of the largest markets for semiconductors and AI-related hardware. Any escalation in restrictions could pressure earnings for major chipmakers while simultaneously accelerating domestic Chinese investment into alternative technologies.

At the same time, the United States continues investing heavily in domestic semiconductor manufacturing through industrial policy initiatives aimed at reducing reliance on foreign supply chains.

This geopolitical competition is creating both risks and opportunities for investors.

On one side, rising tensions could increase volatility across technology stocks and disrupt global manufacturing. On the other, government-backed investments into AI infrastructure, semiconductor fabrication, and strategic industries could create long-term growth opportunities across multiple sectors.

Iran Negotiations Push Oil Markets Higher

While investors monitor U.S.-China relations, energy markets are reacting to growing uncertainty surrounding Iran negotiations.

Recent reports from Reuters indicate that stalled diplomatic discussions involving Iran have increased concerns about future oil supply disruptions and regional instability in the Middle East.

Oil prices have climbed as traders assess the possibility of tighter global energy supply conditions.

For markets, energy prices remain critically important because oil directly influences inflation, transportation costs, manufacturing expenses, and consumer sentiment.

If crude prices continue rising sharply, inflation pressures could remain elevated longer than expected, complicating Federal Reserve policy decisions.

This is particularly significant in 2026 because markets are still debating when and how aggressively the Fed may eventually cut interest rates.

Higher energy prices could delay monetary easing by keeping inflation stubbornly elevated. That would likely pressure growth stocks and highly valued technology companies that have benefited from investor optimism surrounding AI-driven earnings growth.

At the same time, energy producers and oil-related equities could benefit from stronger commodity prices.

This divergence is creating a fragmented market environment where investors are balancing bullish AI momentum against rising macroeconomic and geopolitical risks.

Why Geopolitics Matters More Than Ever for Investors

The modern investment landscape is becoming increasingly shaped by geopolitical strategy.

Historically, investors often viewed political developments as temporary market distractions. Today, however, geopolitics is directly influencing inflation, industrial policy, commodity supply chains, and technological leadership.

For example:

- AI restrictions affect semiconductor earnings.

- Trade negotiations influence manufacturing costs.

- Middle East tensions impact oil prices and inflation.

- Strategic mineral policy shapes battery and electrification markets.

- Taiwan-related risks influence global semiconductor supply.

This interconnected environment means political events now have direct financial consequences across equities, commodities, and currencies.

BlackRock, Goldman Sachs, and McKinsey have all recently emphasized geopolitical fragmentation as one of the defining investment themes of the decade.

Companies are increasingly restructuring supply chains, diversifying manufacturing hubs, and investing in domestic production capacity to reduce geopolitical exposure.

That trend is accelerating investment into sectors such as:

- U.S. semiconductor manufacturing

- Energy infrastructure

- Defense technology

- Cybersecurity

- Critical minerals

- Industrial automation

For investors, geopolitical awareness is no longer optional — it has become an essential part of market analysis.

Future Trends Investors Should Watch

Several major developments are likely to shape investor sentiment throughout the remainder of Q2 2026.

First, investors should closely monitor any outcomes from Trump-Xi discussions involving AI restrictions, trade tariffs, and semiconductor policy. Technology stocks may react sharply to any signals regarding export controls or supply-chain cooperation.

Second, oil prices remain one of the most important macroeconomic variables. Escalating Middle East tensions or breakdowns in negotiations involving Iran could trigger further commodity volatility and inflation concerns.

Third, semiconductor and AI infrastructure companies will continue facing geopolitical scrutiny as governments prioritize technological self-sufficiency and national security.

Fourth, investors should pay attention to strategic mineral policy, particularly involving rare earths, copper, and battery materials. Access to these resources is becoming increasingly tied to industrial competitiveness and defense policy.

Finally, Federal Reserve policy remains deeply connected to geopolitical developments. Persistent inflation caused by energy or supply-chain disruptions could delay expected interest rate cuts and impact broader market valuations.

Key Investment Insight

Geopolitics is becoming one of the most powerful forces shaping global financial markets. The combination of U.S.-China tensions, AI competition, semiconductor restrictions, and Middle East instability is influencing everything from inflation and oil prices to technology valuations and supply-chain strategy.

For investors, this environment creates both risks and opportunities.

Technology, semiconductor, energy, defense, and critical mineral sectors are likely to remain highly sensitive to geopolitical developments throughout 2026. Investors should expect increased market volatility around trade negotiations, AI export policies, and commodity markets as governments compete for economic and technological leadership.

At the same time, long-term structural investment themes tied to AI infrastructure, domestic manufacturing, energy security, and supply-chain resilience may continue attracting institutional capital.

Navigating this increasingly interconnected global market requires staying informed on both economic and geopolitical developments. Follow MoneyNews.Today for daily investor insights, market analysis, and breaking financial news shaping the future of global investing.